The AI-Native P&L

March 19, 2026

Much has been written about the death of SaaS. I believe SaaS won’t die, it will evolve. The dinosaurs will become extinct, but survivors will either be founded as or evolve into AI-Native birds. Just like dino-DNA is different from a bird’s DNA, the P&L of an AI-native SaaS company is going to take on an entirely different shape than its extinct cousins.

I realized this while building the go-forward 4 year financial model for Roam and I am stunned with how much we are going to accomplish for so little compared to what I did before at Yext. Here’s my convictions on the “AI-Native P&L”.

“The cost of software is going to zero, and the cost of acquisition is going to ∞”

-Shutterstock Founder Jon Oringer

R&D. As the cost of software goes to zero, R&D will stay flat over time. You may have a few engineers. Maybe they are 10x engineers. With AI they just became 1000x engineers. What this practically means is that R&D cost will essentially be fixed within a company’s lifecycle. You don’t need to hire more engineers as you grow your revenue.

Traditionally, companies have had to make the tradeoff between maintaining existing features and building new ones. This tradeoff no longer exists. AI Native companies can do more of both, for the same cost.

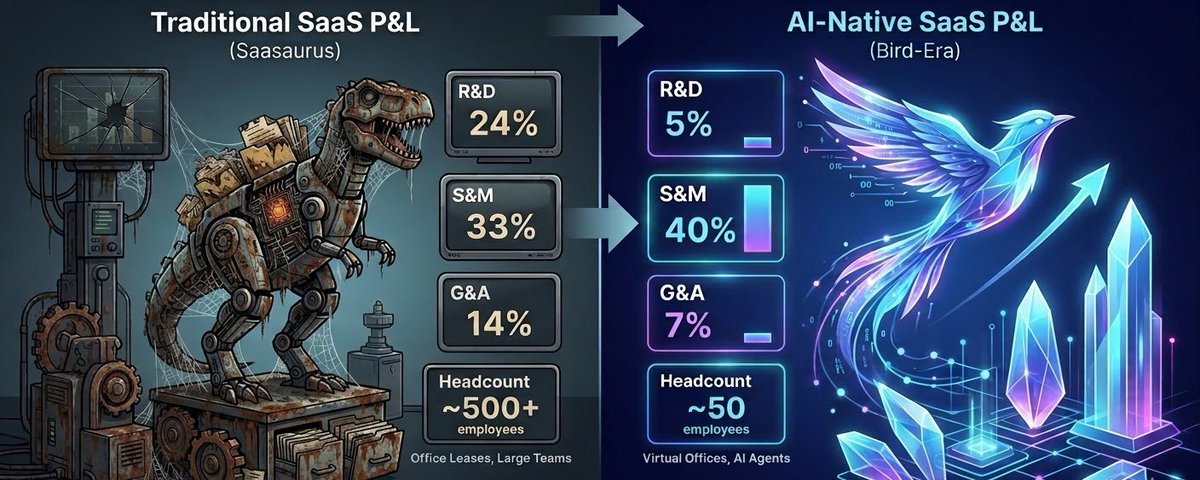

The latest SaaS benchmarking shows an average R&D spend of 24% at IPO. This will be much lower - 5-10% depending on how much you want to build.

R&D Bottom Line: 24% → 5%

Sales and Marketing. Salesforce spent 37% of its Revenue on sales and marketing, Hubspot 49%. The average $100m Saas Company spends 33%. It’s getting easier to make things. This leads to crowded markets. Traditional paid channels become expensive. I predict this goes up. Relationship-led sales can’t be replaced by AI Agents. And, companies will have extra money saved from R&D leaving extra budget to invest in growth. There will be a premium on customer acquisition.

S&M Bottom Line: 33% → 40%

G&A and Headcount. There’s been a lot of talk of the single person unicorn. I think this will happen. But most companies will need people, just way, way less people. I think Roam will get to $100m of ARR on just around 50 people, many entry level. That’s 1/10th of the number of people we needed at Yext to hit the same number. Most will report directly to me. At least I’ll know every person and what they’re supposed to be doing. This is an astonishingly low number. No middle management, less lines of random specialized ops roles, no “customer success”, less legal, less HR people. The fewer people you have, the fewer people you need to support them.

Also, there will be no office space expense. Roam spends exactly $0 on office space. At Yext we spent $20k/year on office space per person on leases alone, notwithstanding all the other stuff that came with it. No AI-Native company of the future is going to get locked down in long-term inflexible leases. They will hire sparingly, for the best cost and highest quality, and build in virtual offices. A physical office is not even AI-native.

The average Saas company G&A is 14% at IPO.

G&A Bottom Line: 14% → 7%.

Cost of Goods. 80% was always the dream margin, the average SaaS pubco is about 72%. Infra will remain the same, but cost of goods also includes customer service heads. AI will replace a huge part of this.

However, I believe companies will build so much AI as a feature into their products that the customer support savings will end up being a wash as spend goes to the foundation models.

Gross Margin Bottom Line: 75% → 75%

Revenue We’ve thus far discussed the expense side, let’s look at the revenue side for a moment. In a crowded market, I think companies with lower, simple pricing will have an advantage. So Revenue will be a bit harder to come by. I also think companies with large surface area have a big advantage over those with a narrow focus. I wouldn’t want to be the CEO of a Premium priced niche SaaS company with a traditional heavy P&L right now.

Also, long term multi-year contracts will be much harder to come by. Why would a big company commit in an era with rapid change?

This may not impact revenue, but it will drive down upfront cash collection and deferred billings.

Concluding Thoughts The SaaSosouruses will become extinct, but the evolved survivors will thrive as birds in their new lightweight form. They will be smaller, more nimble, and arm blooded. And, they have the opportunity to be more profitable.

AI-Native companies may not get as big as they did before, but there will be way more of them, and they will be more profitable.

It’s easier than ever to build. Just do it this new way so you build a modern car (faster and cheaper), not the old fashioned horse and buggy (slower and more expensive).

Bottom Line: +10-15% net margins realized